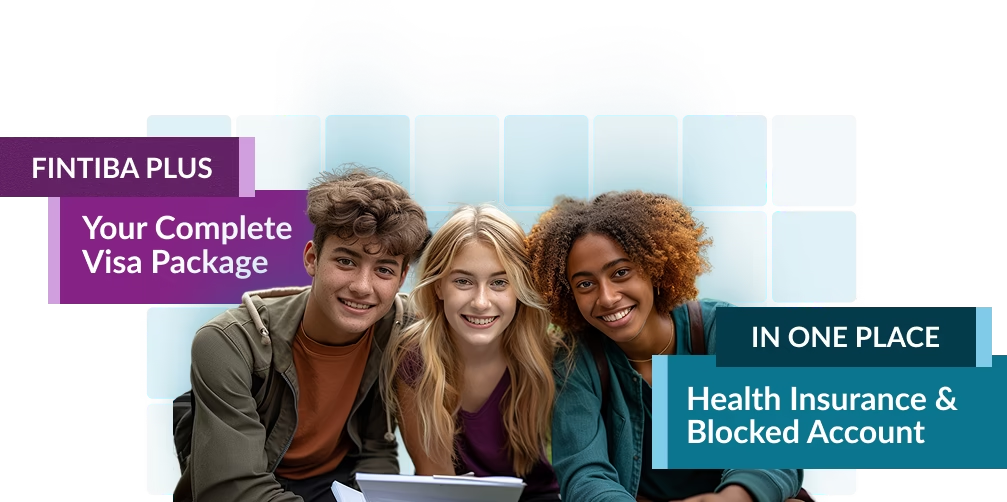

Health Insurance for Students in Germany

Find the right health insurance plan tailored for university students, Studienkolleg students, or language students. Insure your health and well-being while studying in Germany. With Fintiba Plus, you get everything you need for your visa in one simple package.

Health Insurance for Students in Germany

Health insurance for university, Studienkolleg, and language students in Germany. Fintiba Plus gives you everything you need for your visa in one package.

We have collaborated with exceptional partners to ensure that your journey to Germany is effortless.

Health Insurance Options for International Students

Health insurance is mandatory for studying in Germany and is required for both your visa application and university enrollment. Which option you need often depends on your study type and age. Fintiba helps you understand your options and choose the right health insurance for your studies — whether you need public or private health insurance.

Studienkolleg and Language Students

If you are attending a preparatory course before starting university, you are not yet eligible for public health insurance. Therefore, you will need private health insurance for this phase of your stay in Germany.

University Students Under 30

If you are a student under 30, public health insurance is usually the standard option. It provides recognised coverage for your studies and supports your university enrolment through digital insurance confirmation.

University Students Over 30

If you are over 30, the reduced public student tariff no longer applies. You are still be able to stay in public insurance voluntarily, but private health insurance may be a clearer and more cost-effective option for your studies in Germany.

Health Insurance for Studienkolleg and Language Students

You will need private health insurance as you attend your preparatory course. Once you offically begin your university studies, you will be required to switch to public insurance.

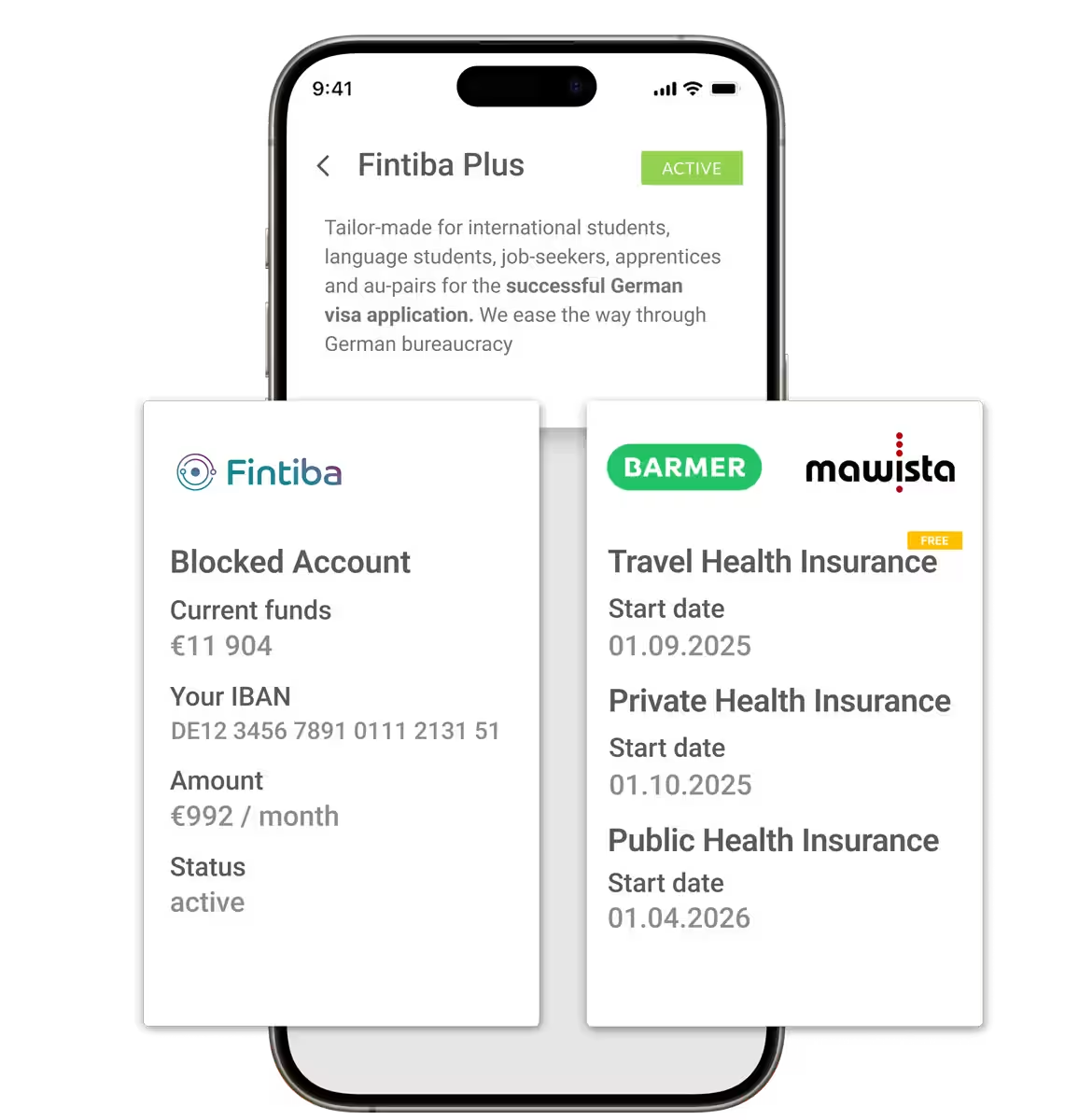

The Fintiba Plus Package provides a complete solution for you. This ensures that you have the required insurance coverage for your visa application, preparatory course, and university studies – all in one bundle.

The Fintiba Plus package includes:

Mawista Student (Private health insurance)

BARMER (Public health insurance) - for the time after students complete their preparatory courses and start university studies

Mawista Visum (Travel health insurance) — provided free of charge

Blocked Account - the embassy required amount for the student visa is €992/month for 1 year (as of 2026). The amount may vary depending on individual cases.

Customer testimonials

Health Insurance for Students Under 30 Years Old

International students under 30 years old who start their studies at a German university typically opt for public health insurance. Fintiba offers public insurance in cooperation with BARMER, one of the largest health insurance providers in Germany.

For university enrollment, students are required to provide an insurance confirmation. This confirmation is sent electronically (M-10 notification) directly from the insurance company to the university.

With the Fintiba Plus Package, students do not need to contact BARMER themselves. Once you provide the name of your university and upload your acceptance letter, all communication between BARMER and the university is handled automatically.

The Fintiba Plus Package for students under 30 includes:

Blocked Account (the embassy required amount for student visa is €992/month for 1 year, as of 2026)

Mawista Visum (Travel health insurance)

BARMER (Public health insurance activated at the start of the semester)

Get Fintiba Plus Today

Fintiba Plus is everything you need for your student visa in Germany — fast, simple, and reliable. One package covers your Blocked Account, student health insurance and you get free travel health insurance, so you can focus on your studies.

Health Insurance for Students Over 30

International students in Germany over 30 typically opt for private health insurance. This is because you are no longer eligible for the public health insurance student rates. You may still remain in public insurance voluntarily, but this is often very expensive. Therefore, it is more affordable and convenient to get private health insurance designed for students.

Within the Fintiba Plus Package, you are automatically guided to choose private insurance. Students can select between Mawista Student and Mawista Expatcare Comfort, depending on their coverage needs.

If needed, they can request an M-10 confirmation from BARMER directly through the Fintiba app.

The Fintiba Plus Package for regular students over 30 includes:

Blocked Account - the embassy required amount for student visa is €992/month for 1 year (as of 2025)

Mawista Visum (Travel Health insurance)

Mawista Student (Private Health Insurance)

What’s Included in Fintiba Plus?

Fintiba Plus brings together the key essentials international students need for Germany: a Blocked Account, travel health insurance, and the right long-term health insurance option based on your study type and age. This helps you prepare for your visa, arrival, and university enrolment with clarity and confidence.

German Blocked Account

Get your required proof of funds ready for your student visa — quickly, securely, and fully online with Fintiba.

Free Travel Health Insurance

Travel health insurance is madatory for a successful visa application. Get it for free with the Fintiba Plus package.

Health Insurance Tailored for You

Get guided to the right long-term health insurance option based on your individual situation.

Everything in One Place

Manage your setup, documents, and important next steps through the Fintiba app and always know what to do next.

Public or Private Health Insurance for International Students in Germany

Choosing between public and private health insurance is a key decision. Both options have advantages but differ in cost, coverage, and eligibility.

Which Type of Health Insurance Do I Need?

Choosing the right health insurance is crucial for your studies in Germany. Understand your options based on your age and student status.

Public Insurance

Suitable if you are under 30 and enroled in a degree programme at a university.

Private Insurance

Required for language students, preparatory courses, or students over the public insurance age limit

Get Fintiba Plus Today

Fintiba Plus is everything you need for your student visa in Germany — fast, simple, and reliable. One package covers your Blocked Account and Health Insurance, so you can focus on your studies.

Can I Switch Between Public and Private Insurance?

Switching from Public to Private Insurance

Students can switch from public to private insurance within the first three months of enrolment by applying for an exemption. After this period, switching is no longer allowed during studies.

Switching from Private to Public Insurance

Switching from private to public insurance is generally not allowed during your studies—even if you start a part-time student job.

A return to public insurance is only possible in case of a major status change, such as starting full-time employment after graduation.

Switching Between Public Insurance Providers

Once you choose a public health insurance provider, you are required to stay with them for at least 12 months. After this binding period, you may change to another public insurer.

Public Health Insurance for International Students

For most international degree students, public health insurance is the standard choice. It provides reliable coverage at an affordable, regulated price.

Who Is Eligible for Public Health Insurance?

Students under 30

Eligible for public health insurance if enrolled at a recognised German university.

Students within the first 14 semesters

Eligible for public health insurance if under the semester limit at a recognised German university.

How Much Does Public Health Insurance for Students Cost?

In 2026, public health insurance costs between €140 and €155 per month, including long-term care insurance. The cost baseline is set by law and rates are similar across all public insurers.

What Does Public Health Insurance for Students Cover?

Public insurance covers:

✅ Doctor visits

✅ Hospital treatment

✅ Mental health care

✅ Prescriptions

✅ Preventive check-ups

It ensures comprehensive protection for essential medical services.

Private Health Insurance for International Students

Private health insurance is necessary for students who do not qualify for public insurance. It provides flexibility and plans tailored to individual needs.

When Do You Need Private Health Insurance in Germany?

International students usually need private health insurance coverage when they:

• Are over 30 years old;

• Are enroled in language courses or preparatory programmes;

• Voluntarily choose private insurance for extra services.

What Is the Cost of Private Health Insurance?

The price of private health insurance varies depending on the provider and selected plan:

• Basic student plans: start at around €95 per month

• Comprehensive plans: can exceed €100 per month

What Does Private Health Insurance Cover?

Private insurance may cover:

• Outpatient and inpatient medical treatment

• Emergency medical services

• Dental care (optional in some plans)

• Alternative treatments (if included)

Health Insurance Requirement for Student Visa Application

All international students applying for a German visa must have valid health insurance. Proof of insurance is a mandatory part of the visa application.

Why Is Health Insurance Mandatory for a German Student Visa?

It ensures that international students are treated on the same basis as residents when it comes to healthcare access. Having valid health insurance is part of the legal conditions set by German immigration law for granting a student visa. Without this proof, the visa application will not be approved.

What Insurance Confirmation Do I Need for My Visa?

The confirmation states that you have sufficient health coverage for your stay in Germany. Without this proof, the German consulate or embassy will not approve your visa application, as valid health insurance is a mandatory condition under German immigration law. Along with insurance documents, embassies require blocked account confirmation as proof of financial resources.

Fintiba Plus includes both essential types of insurance for international students. With one package, students receive travel health insurance for the visa application process and their journey to Germany. At the same time, they get a confirmation of application for either public or private health insurance – depending on their age and student status – which ensures they are covered from the moment they arrive in Germany.

Get Fintiba Plus Today

Fintiba Plus is everything you need for your student visa in Germany — fast, simple, and reliable. One package covers your Blocked Account and health insurance, so you can focus on your studies.

Health Insurance for University Enrollment

Health insurance proof is required by German universities to confirm that students have adequate healthcare coverage. Without this proof, enrollment is not possible.

What Insurance Proof Do German Universities Accept?

How Fintiba Supports the M10 Process

Fintiba provides solutions for both types of students:

- Public health insurance: If you're insured through BARMER via Fintiba, the M10 is sent automatically to your university after you upload your univerity admission letter.

- Private health insurance: You can initiate the M10 notification directly from the Fintiba app or contact BARMER under welcome@barmer.de

Can I Change Insurance After Enrolment?

How to Apply for Student Health Insurance in Germany

Before starting studies, students must arrange health insurance that meets German standards. The steps differ slightly depending on the type of insurance chosen.

Steps to Apply for Public Health Insurance

- Choosing a statutory provider (e.g. BARMER)

- Applying online or at a local office

- Submitting your admission letter, personal data and your German address

- Receiving a confirmation from your health insurance company

Public health insurance usually activates with the semester start date.

Steps to Apply for Private Health Insurance

- Select an approved private insurer offering student plans (e.g. MAWISTA)

- Complete the application form and submit required information

- Enter your payment details

- Obtain confirmation of coverage for enrollment and visa application

Private insurance activation date is defined by the customer. For visa purposes the start date should be the day when you enter Germany unless you also have a travel health insurance. Everyone who resides in Germany should be insured.

Frequently Asked Questions about Student Health Insurance in Germany

Many international students have questions about health insurance requirements and options in Germany. This section answers the most common queries to help you understand your obligations and make informed decisions before starting your studies.

Why do I need health insurance in Germany?

Health insurance in Germany is mandatory by law for all residents, no matter the duration of their stay. But aside from the legal obligation, having health insurance ensures you have access to healthcare services, and you are protected against financial risks. With health insurance, you're covered for any health emergencies or injuries, and do not have to pay for medical bills out of pocket, which can be very expensive in Germany.

What is the M10 digital notification? Does Finitba send the M10 notification about my health insurance status?

M10 is the notification about the status of your health insurance. In Germany, health insurance providers and universities are obliged by law to notify one another of students' health insurance status. Regardless of which kind of health insurance you have, you must contact one of the public health insurance providers to initiate your M10 digital notification prior to enrolment. Every student who obtained health insurance within Fintiba Plus can now complete this process directly from the Fintiba App.

Is student health insurance mandatory in Germany?

Yes, health insurance is mandatory for all students in Germany. Without valid health insurance, students cannot enroll at a university or apply for a visa or get the residence permit.

Can I apply for health insurance from abroad?

Yes, both public and private health insurance applications can usually be completed online from abroad, depending on the provider you choose. This allows students to have proof of coverage before arriving in Germany.

How long does it take to get health insurance confirmation?

The confirmation letter is typically issued within a few days of submitting your complete application. Many providers send it electronically for faster processing.

Can I change from private to public insurance during my studies?

Changing from private to public insurance during your studies is usually not allowed. An exception applies if your status changes, for example, if you start a job that requires public insurance.

Can I use health insurance from my home country?

In most cases, no. Health insurance from your home country is not accepted unless it meets German legal standards and you obtain an official exemption from public insurance. EU students with a valid EHIC card may use it temporarily.

Does student health insurance cover dental treatment?

Yes, public health insurance generally includes basic dental care, such as check-ups and fillings. Private insurance coverage for dental treatment varies depending on the plan; some offer extended dental services.